This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

<== Our conclusion was that this isn’t a temporary blip that will swiftly trend-back up in a V-shaped recovery of valuations but rather represented a new normal on how the market will price these companies somewhat permanently. We’ll just wait until companies that last raised in 2019 or 2020 come to market.”

2 preamble issues having read the comments on TC today: 1: I know that the prices of startup companies is much great in Silicon Valley than in smaller towns / less tech focused areas in the US and the US prices higher than many foreign markets. You can be pissed off, but I don’t set prices. That’s stupid.

When convertible debt first started being introduced as a “faster, cheaper way to get startups funded” they didn’t have pricing built into them. A standard entrepreneur retort I heard back then (2008-09) was “I don’t know what my company is worth now. They’ll get priced soon enough by a VC.”

VC firms see thousands of deals and have a refined sense of how the market is valuing deals because they get price signals across all of these deals. As an entrepreneur it can feel as intimidating as going to buy a car where the dealer knows the price of every make & model of a car and you’re guessing at how much to pay.

I am chairman of a company that, as I write this, is twelve years old and has not yet taken a dollar of outside investment. The company has been funded entirely by grants from the National Institute of Health, amounting to millions of non-dilutive dollars in all. Grant writing takes skill and immense amounts of time.

Today we’re in a world where 10 accelerators are bombarding you with emails to meet their 10-15 companies. Of course these are great places to network with other investors, meet great entrepreneurs and keep your connections strong with senior execs at larger companies like Yahoo!, They worry too much about missing out on a deal.

Prorata investments rights given investors the right to invest in your future fund-raising rounds and maintain their ownership % in your company as your company grows and raises more capital. New investors sometimes want early investors to put in money to “prove” they have confidence in the new price.

I got a call from a VC friend of mine who said, “we’re looking at this deal but can’t write the full check. But I had just seen the company present at a recent tech event and thought highly of what they were building. I was interested in the company but I wasn’t chasing the deal.

How did you determine the right price points for your product? Like many companies they experimented with many pricing models. They tried lots of price points – $13.99, $9.99 When they increased price from $9.99 My key take away – frame of reference in pricing is important. Gregg says at $9.99

Like it or not – finance is a major job function in any company – startup or public company. The profile of one of the hottest companies I met was as per the graph below. But I really think this company has a good shot at becoming a monster. Investors are writing checks for dots.

What price? Because entrepreneurs often went to lawyers at their earliest stages to get their company registration done. I tapped my friends at big tech companies (Salesforce, Google, Oracle). The only way for a company to be overvalued is if there’s someone willing to pay that price. What stage? I hustled.

What price? Because entrepreneurs often went to lawyers at their earliest stages to get their company registration done. I tapped my friends at big tech companies (Salesforce, Google, Oracle). The only way for a company to be overvalued is if there’s someone willing to pay that price. What stage? I hustled.

.” In the article I discussed the downside of raising capital at a too high of a price and referred people to a previous article I had written encouraging founders to raise “ At the Top end of Normal ” as opposed to stratospheric prices. First, a down round sends a signal that something is wrong with your company.

…” I’ll write soon on my views of why I believe Instagram took off as a social network and what I think comes next. What I want to talk about today is one of the insider baseball discussions of our industry this past week: The odd fact of the $500 million financing round completed just before the company sold for a B.

Back in 1999 when I first raised venture capital I had zero knowledge of what a fair term sheet looked like or how to value my company. Other founders, “as a privately held company we don’t disclose our valuation.&# Me, “dude, I’m not a journalist. The VC assumes you’ll have an option pool.

I find it amusing when a journalist writes an article about a prominent startup (either privately held or preparing for an IPO) and decries that, “They’re not even profitable!” Exec Summary: Most companies (98+%) in the world (even tech startups) should be very profit focused. One of them is profitability.

Some objections are real and they end up becoming changes to your product, your service plan or your pricing / bundling. As a founder, when you’ve been dealing with these kinds of objections for a couple of years it becomes natural and you easily handle objections on price, product & competition without much thought.

When you first start your career as an investor (or when you first start writing angel checks) your main obsession is “getting into great deals.” They sold 2 years later for $16 million In the financial crisis of 2008 we had a company that had jointly hired lawyers to consider a bankruptcy and also pursued (and achieved!)

Nor do they exist in the investors of early-stage companies. I’ve started writing up some of those sales & marketing lessons and I plan to continue to build that section out over time. Many great ones don’t thrive in the early phase of a company where the sales is more consultative or evangelical.

Yesterday I saw a Tweet from Chris Sacca fly by that prompted me to want to write a blog post helping entrepreneurs understand why they should push back against VCs asking for “super pro-rata” rights. Obviously the situation is very different in companies where the company isn’t “killing it.”

I explain in the video what happened in my first company (e.g. on the entrepreneur side of the table) when I raised at too high of a price. Down rounds are psychologically really difficult on companies and can make it harder to do later rounds. Pricing high also takes exit options off the table.

As a result I’ve really resisted writing about negotiations. Sometimes I even say, “I will change price / terms if I need to. If I forget to write, “Don’t Negotiation Piecemeal” after that then remind me. Your job is to offer a price (or terms) and walk. submitting term sheets.

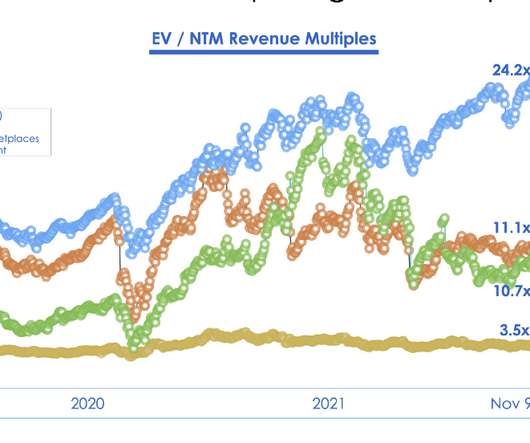

There is much discussion online and also in small, private groups, about why the price of technology companies – public and private – are falling. Valuing any company can be difficult because it requires a degree of forecasting future growth & competition and ultimately the profits of the organization.

Brad is also the Co-Founder of TechStars , an acclaimed startup boot camp which has spawned a number of promising companies. Of the 80 companies that have completed the program since its 2007 inception, 49 have received funding, 8 have been acquired and 8 have ceased operations. Writing a book is very different from writing a blog.

I wrote my version here and Scott wrote an excellent write-up of his views here. We both agree that the later-stage valuations are being driven up to a point that feels irrationally priced [he uses b-round SaaS valuations as an example and I am willing to be even more broad based]. Each of the two videos is about 10 minutes long.

There is a transition in every company from a “seat of the pants&# kind of entrepreneurial company to a “process driven&# mechanized one. Frankly, I’m much more of the former kind of guy and I tire of the routine process & politics required to succeed in a big company. This seldom works.

I pointed to several Economist articles I had read that mapped historical prices of real estate for 400 years and how on average property values grow at no more 1.5% above inflation yet in many markets in the US & Europe prices were rising at 10-25% per year. And it’s driving up prices beyond their inherent value.

I started by writing 3-4 times / week. I didn’t have any grand ambitions other than to write, share ideas and try to build awareness of who I am through my thoughts. I agreed to finance a company today. If I get a holiday bump I’ll raise a round at whatever price I like. I’ve kept it up for 2 years.

The truth is I have been thinking a lot about the topic, I just haven’t been writing about it. AWS helped lower the cost of starting a company by 90%. When I started my first company at 31 year’s old I had to raise at least $5 million. million to launch a SaaS software company and we took $2.5

This happens when the company has been making steady progress but hasn’t built enough “ proof &# to raise its next round of financing from external investors. If no financing happened then this “note&# may not be converted and thus would be senior to the equity of the company in the case of a bankruptcy or asset sale.

I will write more about this in the next 2 weeks. As any historian of bubbles will tell you – there were periods of bubbles in assets as arcane as tulips , South American trading companies , dot-com bubbles & housing bubbles. Ah, but today’s Internet companies have real revenue! I believe that. and profits!

I was speaking recently to the team at NuOrder , an LA-based company we’re an investor in about “realism in startups” — an impromptu talk I have given to any of our portfolio companies who ask. I answered in the same way I always do so I thought I’d just write it publicly. “I I work with a few computer vision companies.

Preparing for the game… If you have been following our recent insights, you’ll be up to speed knowing that professional investors negotiate tough terms, from provisions of control over asset acquisition, eventual sale of the company, future investments, forced co-sale when others attempt to sell their shares and more.

It’s true the some VCs have started writing so many checks that they resemble stock pickers but the majority of us still have less than 10 board seats at any time and tend to go pretty deep so the result is that we care deeply about where we commit our time. Could we produce this at cost? It was impressive. Upfront Ventures'

When to get a lawyer - If you plan to be a venture or angel backed technology company (what I mostly write about) the best time to start meeting and getting to know lawyers is long before you ever start your company. Many people start companies arse backwards. Shame about that pesky FAS 157 ruling.

I give a sneak peek at a blog post I’m writing on the topic next week. Convertible debt is a loan to the company that doesn’t typically get paid back but rather “converts&# into equity when you raise a larger round at a later date. I’m going to make this a regular part of the show since it was really fun.

The prices of angel deals have recently crept up, VCs have also gotten their checkbooks out again, frothy deals are happening and people are feeling bullish. VCs have also gone back to writing checks because as an industry we can’t be seen as “sitting on the sidelines” for years at a time. VCs get paid to “put money to work.&#.

The Facebook parent-company saw its stock price get bludgeoned after a bad earnings report showcased that Apple’s ad-blocking changes are shaving billions off its books and the company’s crown jewel — the Facebook platform — has stopped growing and actually shrank this quarter.

Will Price , October 11, 2010 Georgians Should Vote No - Force of Good: a blog by Lance Weatherby , October 28, 2010 Free Software for Managing a Lean Startup - Platforms and Networks , January 17, 2010 Purpose Driven Life - Journey of a Serial Entrepreneur , July 26, 2010 Two Decade-Defining Acquisitions?

If you know, VCs end up writing sizable checks into their own funds, which is important in better aligning interests. They will have to negotiate price and terms. M&A discussions (where your company is buying or being bought). million round I might write $1.8 – 2.2 This is the same way VC firms, by the way.

The company said the software now supports automated check writing and electronic vendor or owner payments in the software, including full service check procesisng where it prints and mails checks for businesses. Pricing on the new features were not announced by the company. READ MORE>>.

We short-handed this marketing mix as “ the four P’s ” – product, price, promotion and place (distribution) – this was devised in 1960 and while a little bit dated is still a useful framework. Online marketing uses techniques for driving promotion and place. Look at Viddy & SocialCast.

If you have been following our recent insights, you’ll be up to speed knowing that professional investors negotiate tough terms, from provisions of control over asset acquisition, eventual sale of the company, future investments, forced co-sale when others attempt to sell their shares and more.

We had the final terms of our agreement fairly well boxed in within a range of about 5-7% on price and within 30 days on move-in date. I obviously preferred the lowest price and I wanted the latest move-in date. She told me, “start with the price you want but the move in date he wants.&#. I told my agent. She way annoyed.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content