This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

How do you value pre-revenue companies? Last time we examined ten different ways to value companies already in revenue, usually beyond the early stage. For those of us who’ve invested in early-stage companies, especially technology startups, we have confronted a universal problem.

He wants to compete to be the lead drummer in the competitive ensemble and study under Terence, an obsessive instructor who is hell bent on winning competitions for the school. But the film has my brain buzzing all week about obsessive and competitive people. I absolutely loved the film. I loved the music. We revere musicians.

This week I wrote about obsessive and competitive founders and how this forms the basis of what I look for when I invest. I had been thinking a lot about this recently because I’m often asked the question of “what I look for in an entrepreneur when I want to invest?” I had invested in myself for years.

For those of us who’ve invested in early stage companies, especially technology startups, we have confronted a universal problem. There are many ways to project the value of a company for purposes of pricing an investment, but all rely upon the revenue and profit projections of the entrepreneur as a starting point.

Portfolio company support & analysis. Associates often shadow partners at board meetings so that they can help follow up with the company on important initiatives between board meetings. Most associates need some entrepreneurial experience before actually making investments. Portfolio community building. Industry reviews.

I was speaking recently to the team at NuOrder , an LA-based company we’re an investor in about “realism in startups” — an impromptu talk I have given to any of our portfolio companies who ask. During the Q&A I was asked about how I make investment decisions in early-stage businesses. I fall in love.”

I was at a dinner recently in Chicago and the table discussion was about building great companies outside of Silicon Valley. It’s not the great companies you build, it’s the silent killer of those that should have been build locally and weren’t. Klout was an LA company – sold for $200 million to Lithium.

He was a life-long entrepreneur and the first business he created out of college (actually, he founded it while he was at Caltech) was a company that manufactured high quality audio speakers. So he launched a company with exclusively paid search. They were a juggernaut and Google was a small company. Overture was sold to Yahoo!

And good board members can add real value to you and the company. But sometimes there is a barrier, an impossibly high cost not considered, a social backlash never thought of, or competition already covering the idea that is unknown to the originator. Strategic thinking: Board members who ask: “What is the competitive landscape?”

Last year at this time I spoke at VidCon and gave this presentation in which I said YouTube was “the Walmart of Online Video” but I also commented that I felt YouTube was vulnerable to competition because their rev share to MCNs wasn’t high enough to allow MCNs to build a profitable business inside of YouTube.

Don’t bash the competition. Every investor knows how vulnerable a new startup is to competitors, so investors always ask about your sustainable competitive advantage in the marketplace. That says you are competitive today, have a real barrier to entry, and the potential to remain ahead of the competition for a long time.

Many CEOs have asked me if I felt an investment banker adds value if the buyer has already been identified. How investment bankers behave. Investment bankers sometimes slow the process by requiring a cloud-based “data room” and “deal book” to be prepared containing considerable information about a company to help a buyer.

In case you hadn’t noticed, the key elements of a competitive advantage for your business have changed as businesses move online, and your domain is instantly global. As a business advisor, I have to recommend even to established companies that they review and revamp their competitive strategy now, even if it appears to be working today.

Don’t bash the competition. Every investor knows how vulnerable a new startup is to competitors, so investors always ask about your sustainable competitive advantage in the marketplace. That says you are competitive today, have a real barrier to entry, and the potential to remain ahead of the competition for a long time.

Photo by Vanna Phon on Unsplash Customer acquisition is the lifeblood of many startups from e-commerce to gaming to marketplace companies, among others. For these companies, it looks like a rosy picture. Why Did I Invest in Trust? no surprise?—?that’s that’s where the customers are. founders, marketers, investors?—?and

Know your market and competition, or don’t spend a dime on anything else. In 1994, (I know a long time ago), I invested over a million dollars into a company whose entrepreneurs had a vision that I bought into for many reasons, not the least of which was that I had industry experience and understood the need.

leadership, mentorship, competitiveness, communications, relationship-building?—?and Kara said “no” because she wanted to start her own company, which she did and I backed. Instead he championed our investment themes into sustainability and food technologies having invested in companies like Apeel Sciences and Ynsect.

More importantly, he has just announced his first investment – he led a $7 million investment in Deliv – please read about it on Greg’s spiffy new blog. Another one of his big themes has been B2B crowd-sourcing and he had a company in mind already even before he joined – Deliv. I wrote about him here.

We believe that it is incrementally harder to differentiate on simple Internet products or mobile apps and while great companies are built doing this, our goal as a fund is to try and fund things that can be 100x returns if they work. We’re not Pollyannaish about this. In short, we’re after venture returns.

Competitive (Athlete: skier & rowed at Princeton, hates losing at everything she does). Investment experience (5 years a VC at Battery Ventures). Helped merge company with Seedling – on track to do $20 million combined revenue in 2015 – will now become Chairman). billion IPO), Envestnet (Chicago, $1.25

If fixed expenses, especially payroll, are paid out before cash is received from services or shipments, the company is financing its growth with ever-increasing working capital needs. This is one interpretation of It takes money to make money , although that statement was probably created to describe new investment opportunities.

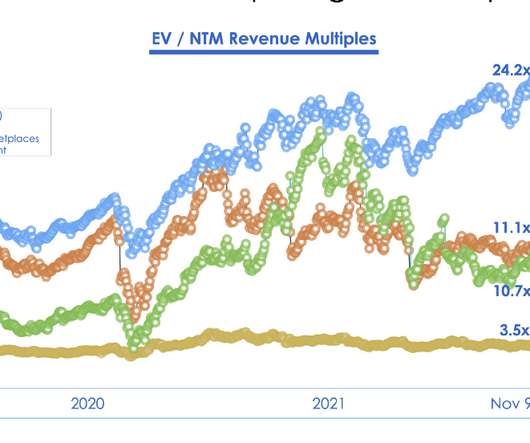

<== Our conclusion was that this isn’t a temporary blip that will swiftly trend-back up in a V-shaped recovery of valuations but rather represented a new normal on how the market will price these companies somewhat permanently. First in late-stage tech companies and then it will filter back to Growth and then A and ultimately Seed Rounds.

2 preamble issues having read the comments on TC today: 1: I know that the prices of startup companies is much great in Silicon Valley than in smaller towns / less tech focused areas in the US and the US prices higher than many foreign markets. There is an inherent value that any company has. I acknowledged this in the article.

An entrepreneur pitches using a deck with no slide for competition. We have no competition.”. That statement has killed more investment deals than almost any other. When asked (as we always do,) the response is “This is new. Professional investors laugh when they hear an entrepreneur come out with that one. Do your homework!

You have to understand whether they’re likely to yield revenue growth in the near term OR whether you have access to cheap enough capital to fund your losses until your investments pay off. Exec Summary: Most companies (98+%) in the world (even tech startups) should be very profit focused. If you don’t, somebody else WILL!”

Creating awareness for your brand and products is one of the lifebloods of technology startups yet in a world where so many companies are being created it becomes difficult to rise above the noise. Ever notice how some companies tend to be in the press all the time and your big new product launch struggled for inches?

And good board members can add real value to you and the company. But sometimes there is a barrier, an impossibly high cost not considered, a social backlash never thought of, or competition already covering the idea that is unknown to the originator. The punch line: Investing in the creation of a governance board is not enough.

The costs to start are much lower than ever (90% reduction in infrastructure costs to start a company through open source & web services) and large companies being created in many geographies. Companies are now raising much more capital in the private markets now before they go public. Thus is a key point.

This morning's interview is with Kevin O'Connor , a longtime investor and serial entrepreneur, who is now running venture capital investment firm ScOp Venture Capital. Kevin sold his last company, Santa Barbara-based Graphiq, in July of 2017 to Amazon, but has a long history of successful companies, including founding DoubleClick.

Scott Kupor of A16Z responded with a comprehensive overview of valuation methodology in a post that while accurate feels more targeted at sophisticated Limited Partners (LPs) who invest in funds. billion (and their stake worth $237 million not $3 billion) — the reported value at which they invested in the last round. We can’t know.

There’s a new company that’s sitting on top of some of the fastest growing consumer-facing businesses in the world — liquor and marijuana delivery — and its name is Pacific Consolidated Holdings Group. Financial terms of the transaction were not disclosed. .”

You can build a meaningful company just about wherever these days. ” Most VCs view it as their responsibility to mentor, debate, cajole and generally assist with investments they make. They also view it as a responsibility of the money they manage on behalf of others to provide oversight of these companies. Not easily.

We sat down with TX Zhuo , who is heading up the firm's venture investments, about the fund and his path here after a recent stint at Eric Schmidt's Innovation Endeavors fund in Palo Alto. We are going to focus most of our investments in LA. We have four investments so far, two of which are public. What is Karlin Ventures?

Wallach on investments out of a new fund, Inevitable Ventures. How did you end up here in Los Angeles doing investments? Coincidentally, that was the exact same time in 2009 when I moved out, when Ashton Kutcher started first investing. Ron chose me to manage those investments. We brought in a third partner, Guy Oseary.

Since Arrested Development is back I thought I’d resurrect Gob Bluth’s answer when he was told he needed a “business model” – he quickly figured out that he was missing one so he asked Starla, the Bluth company secretary, if she would be his business model. You need product / market fit.

In my first enterprise software company we developed a methodology for sales that we called PUCCKA , which I wrote about previously. Having a good sales methodology can help you ensure your company runs more disciplined campaigns and focuses scarce resources on your best opportunities. The first post covered the topic of “P” or pain.

AngelList 101 : As you know, AngelList is a platform where angels can invest in semi-screened tech deals. As an angel you can look for the social proof in deals “Dave Morin is investing …” to make your decision. AngelList Syndicate leads don’t take any fees on the investment, which should help with returns.

I didn’t invest in any of their fine competitors either like Lyft, Sidecar, Hailo, etc. They were a little too fierce in their competitive practices against Lyft to sign up drivers. It’s a brutally competitive world out there because there are extreme amounts of money at stake. I’m not so sure. I wish I were.

They often create the biggest tensions between investors who are investing at different stages in the business. Prorata investments rights given investors the right to invest in your future fund-raising rounds and maintain their ownership % in your company as your company grows and raises more capital.

I will argue that LPs who invest in VC funds will also need to adjust a bit as well. When I built my first company starting in 1999 it cost $2.5 That makes both of these amazing companies great channels for startups. Every startup I knew in 2005 (when I started my second company) was using this. Enter Amazon. Not Google.

Many questioned whether it could survive under the fail whale, inevitable competition from Facebook, founder fighting, fights with 3rd-party developers let alone become a revolutionary business that could make money. ” So other partners at the firm might sling mud at your ideas as you go for approval on an investment. Lots of it.

It’s super hard not to want to spend more time with these companies. For all the things he’s likely known for, he probably hasn’t yet built a strong relationship as an early stage venture investor (he invests often in later-stage deals where he is very respected). Competition is fierce. Why am I so lucky?

Back in 1999 when I first raised venture capital I had zero knowledge of what a fair term sheet looked like or how to value my company. Due to competitive markets we ended up with a pretty good term sheet until we needed to raise money in April 2001 and then we got completely screwed. Investors own 25%, the founders own 75%.

We first met the Chicago-based company and its founder and CEO Vitaly Alexandrov last year when we reported that Food Rocket launched in the Bay Area , going up against the likes of Amazon Fresh, DoorDash, Instacart and Gopuff, which is no easy feat given each of the company’s footprint.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content